Obtaining your first credit card when you have no credit might be challenging, but not impossible, whether you are a student or a newcomer.

Anyone with no credit who wants to acquire their first credit card and start developing their credit history has a lot of possibilities.

It’s crucial to bear in mind the necessity to use your card properly while you consider your alternatives. Using credit cards carelessly may soon defeat the purpose of building your credit history. Continue reading to get the finest advice for selecting and obtaining your first credit card.

What Is a Young Adult Credit Card?

A credit card for young adults is a particular kind of credit card created for college students who are currently enrolled, recent graduates from college, and those who have accepted their first post-college job.

The best credit cards for young people demand a lower credit score than standard cards, have cheaper fees, assist in credit building, and provide incentives. There may even be a credit freeze Canada option on some cards if there are difficulties with the payment. Some credit cards for young people could ask for documentation of your enrolment in an acceptable institution or check your age.

What Distinguishes a Young Adult Credit Card from a Standard Credit Card?

A credit card for young people is created with the first-time full-time employee, recent graduate, and enrolled college student in mind. These three categories have no or little credit history in common.

A credit card for young people often has less stringent credit history restrictions than a standard credit card. For instance, you could need at least three years of credit card management experience to get a standard card, while a credit card for young people might accept you with only a year or perhaps no history at all.

For My First Credit Card, Do I Need a Co-Signer?

For applicants under the age of 21, certain credit card companies may need a co-signer (usually an adult over the age of 21) on your credit card account, while others may not. If you are unable to make your payments, the person you choose to name as a co-signer will also be responsible for any debt incurred.

How Can I Apply for a Credit Card in Canada for the First Time?

During the application process, you may anticipate the following steps:

- Choose the card that works best for you. Consider the advantages, perks, interest rates, and features that may be associated with the various credit card options, and decide which advantages, perks, and features are most significant to you.

- Apply online. When you’re prepared to apply for a credit card, check out the creditor website to learn about your alternatives for submitting an online application.

- Watch for a response. The credit lender will examine your details once you submit your application. You can be immediately approved or rejected depending on your credit history and financial position.

- Carefully read your cardmember agreement after approval. Make sure you are familiar with specifics such as how to use and authenticate your card, how to make a payment, invoicing information, and information on your interest rates.

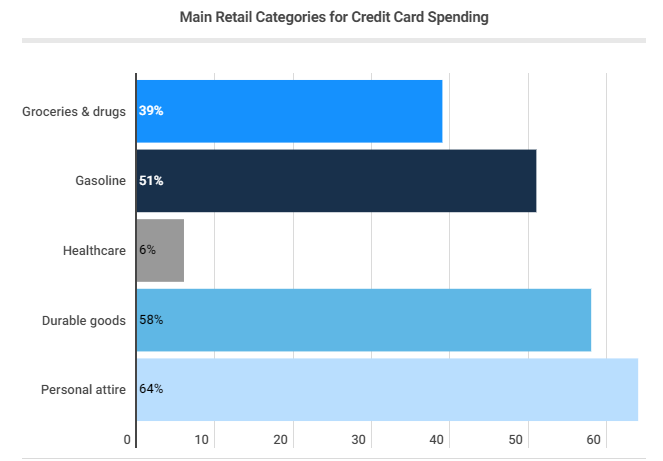

If you’re wondering what you’ll be buying when you get your credit card, take a look at this graph of how Canadians spend with credit cards. Usually, people use a credit card in those cases when it is convenient for them, or they need to pay quickly.

You also need to understand that most credit card spending is due to improving your credit score so you can make bigger purchases and lower interest rates.

You also need to understand that most credit card spending is due to improving your credit score so you can make bigger purchases and lower interest rates.

Choosing Your First Credit Card

There are several credit card options available for young people. There are secured credit cards, cashback cards, rewards cards, and credit cards for college students.

Let’s go through some key characteristics you should consider when determining if a card would meet your financial demands.

Low or No Yearly Cost

It seems sensible that banks, which are for-profit organizations, would need to charge a fee to maintain a product’s profitability. However, many financial institutions may accommodate young people and college students by temporarily eliminating all or a portion of their costs. Keep an eye out for them.

Low-starting APR

The cost that a financial organization charges you for borrowing money is known as the annual percentage rate (APR). A percentage is used to represent the APR. You save more money on fees the lower the APR is!

Minimum Credit Score

Young folks should look for a card that allows a lower credit score for two reasons. First off, it raises your chances of getting your card authorized. If you already have a credit history, it increases your chances of receiving a lower interest rate.

Payback Incentives

Some young adult credit cards provide rewards for all financial outlays, certain qualified purchases, or only a select few categories.

Free Use of Online or Mobile Banking

You can check your spending, balance, and credit card statement history using online banking from many banks and credit unions, as well as set up automated payments. Although online banking is convenient, mobile banking is simpler and quicker.

Service for Free Credit Monitoring

Creating a credit history is one of your key goals in applying for a credit card. You’ll be more driven to make payments on time and be able to see your credit score rise if you have a credit monitoring system that provides you with monthly updates on how you’re performing.

Submitting a Report to Major Credit Bureaus

Verify if the credit card provider you are thinking about reports to the main credit agencies. It’s essential if your goal is to establish credit by applying for a credit card.

How to Obtain a Credit Card When You Have No Credit

Student Credit Card

The best course of action if you’re a student at a college or university is to apply for a student credit card from a bank or other significant credit card provider.

These cards often have high-interest rates and provide nothing in the way of incentives, but they’re excellent stepping stones for developing your credit history and setting you up for a better credit card.

Secured Credit Card

Consider applying for a secured credit card if you are not a student and have no credit history. With secured cards, you make a deposit that is deducted from the card’s credit limit. The lender keeps this deposit just in case you don’t make a payment.

Retail Store Credit Card

Applying for a credit card from a retailer or department store is another choice for a first credit card. Store credit cards are a good alternative for somebody with no credit history since they often have greater acceptance probabilities than most other credit cards.

Gain Authorized User Status

Consider signing up to use someone else’s credit card as an authorized user. It’s critical to comprehend the dangers since, as an authorized user, the card’s activity will also be reflected on your credit report: Your credit history will also reflect any late payments made by the other authorized user.

Conclusion

Now you know the basic information on how to get and choose your first credit card. Now the matter remains small – you need to delve into each of the aspects on your own, apply and start building your path to an excellent credit score.

Become a Harlem Insider!

By submitting this form, you are consenting to receive marketing emails from: . You can revoke your consent to receive emails at any time by using the SafeUnsubscribe® link, found at the bottom of every email. Emails are serviced by Constant Contact